The average cost of homeowners insurance in the United States is $1,290 per year or $108 per month. Homeowners insurance is a critical coverage that virtually all homeowners need to have, with over 85% of homeowners carrying this insurance, according to the National Association of Insurance Commissioners (NAIC).

This insurance coverage provides protection for the cost to rebuild a home in the event it is damaged by a covered peril such as a fire or windstorm, as well as protection for damage to a homeowner’s personal property. Homeowners insurance also provides personal liability protection in the event that a homeowner is sued for causing property damage or bodily injury. Homeowners insurance is often a required coverage when homeowners have an outstanding mortgage.

Average Cost of Homeowners Insurance by State

The cost of homeowners insurance varies widely depending upon the state. While our analysis found that the average cost of homeowners insurance was $1,290 nationwide, the average cost was as high as $1,987 in Louisiana, the most expensive state, to as low as $706 in Oregon, the least expensive state.

| State | Average Monthly Cost | Average Annual Cost | Difference from National Average |

|---|---|---|---|

| Alabama | $117 | $1,409 | 9% |

| Alaska | $82 | $984 | -24% |

| Arizona | $70 | $843 | -35% |

| Arkansas | $118 | $1,419 | 10% |

| California | $89 | $1,073 | -17% |

| Colorado | $135 | $1,616 | 25% |

| Connecticut | $125 | $1,494 | 16% |

| Delaware | $73 | $873 | -32% |

| District of Columbia | $105 | $1,264 | -2% |

| Florida | $163 | $1,960 | 52% |

| Georgia | $109 | $1,313 | 2% |

| Hawaii | $95 | $1,140 | -12% |

| Idaho | $64 | $772 | -40% |

| Illinois | $92 | $1,103 | -14% |

| Indiana | $86 | $1,030 | -20% |

| Iowa | $82 | $987 | -23% |

| Kansas | $135 | $1,617 | 25% |

| Kentucky | $96 | $1,152 | -11% |

| Louisiana | $166 | $1,987 | 54% |

| Maine | $75 | $905 | -30% |

| Maryland | $89 | $1,071 | -17% |

| Massachusetts | $129 | $1,543 | 20% |

| Michigan | $82 | $981 | -24% |

| Minnesota | $117 | $1,400 | 9% |

| Mississippi | $132 | $1,578 | 22% |

| Missouri | $115 | $1,383 | 7% |

| Montana | $103 | $1,237 | -4% |

| Nebraska | $131 | $1,569 | 22% |

| Nevada | $65 | $776 | -40% |

| New Hampshire | $82 | $984 | -24% |

| New Jersey | $101 | $1,209 | -6% |

| New Mexico | $90 | $1,075 | -17% |

| New York | $110 | $1,321 | 2% |

| North Carolina | $92 | $1,103 | -14% |

| North Dakota | $108 | $1,293 | 0% |

| Ohio | $73 | $874 | -32% |

| Oklahoma | $162 | $1,944 | 51% |

| Oregon | $59 | $706 | -45% |

| Pennsylvania | $79 | $943 | -27% |

| Rhode Island | $136 | $1,630 | 26% |

| South Carolina | $107 | $1,284 | 0% |

| South Dakota | $107 | $1,280 | -1% |

| Tennessee | $103 | $1,232 | -4% |

| Texas | $163 | $1,955 | 52% |

| Utah | $61 | $730 | -43% |

| Vermont | $78 | $935 | -28% |

| Virginia | $86 | $1,026 | -20% |

| Washington | $73 | $881 | -32% |

| West Virginia | $81 | $970 | -25% |

| Wisconsin | $68 | $814 | -37% |

| Wyoming | $99 | $1,187 | -8% |

Numerous factors affect the cost of homeowners insurance in various states. Among the most important factors are the impacts of weather and natural disasters such as windstorms, hurricanes, wildfires, snow and hail storms, and other weather factors. Additionally, the effects of crime, the cost of housing construction, and the tort system of legal liability in each state also influence the premiums paid by homeowners. Importantly, earthquake and flood damage is excluded from most homeowners insurance policies, so these factors tend to have minimal influence on the premiums paid for homeowners insurance policies.

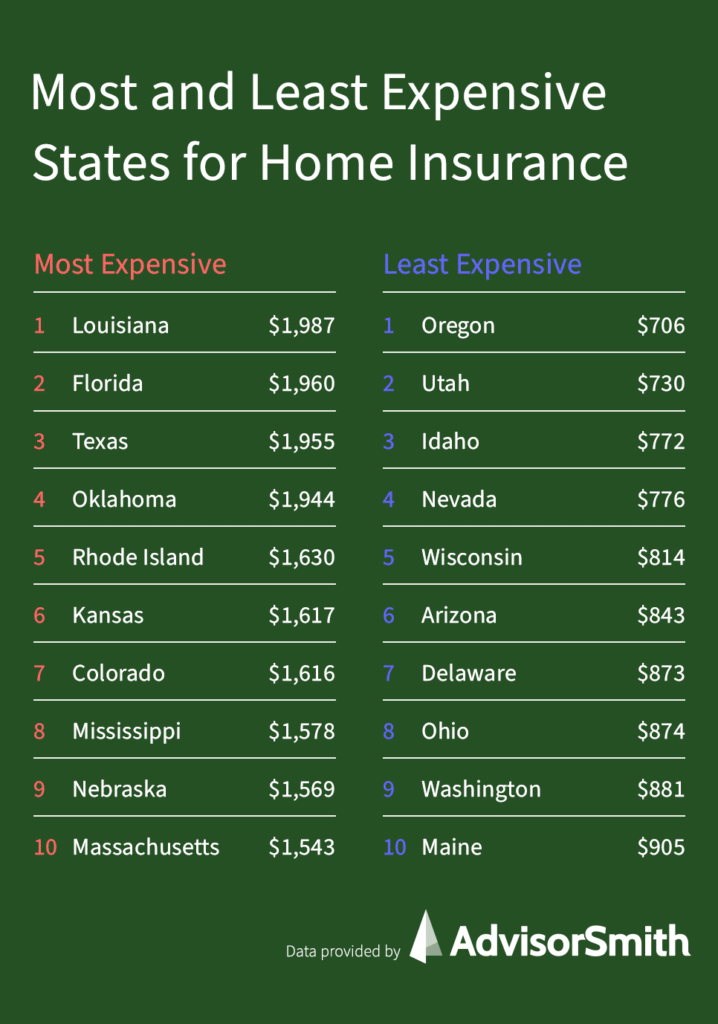

Most Expensive States for Homeowners Insurance

The most expensive states for homeowners insurance were states in the South, with the top four all being Southern states. The rest of the top 10 most expensive states were a mix of Midwestern and Northeastern states. Colorado, a western state, also made the top 10.

The top five most expensive states for homeowners insurance are:

- Louisiana, with an average annual cost of $1,987

- Florida, with an average annual cost of $1,960

- Texas, with an average annual cost of $1,955

- Oklahoma, with an average annual cost of $1,944

- Rhode Island, with an average annual cost of $1,630

The top three most expensive states for homeowners insurance are Louisiana, Florida, and Texas. These three states are some of the most vulnerable states to hurricane and wind damage, with hurricanes coming from the Atlantic Ocean and the Gulf of Mexico on an annual basis. These hurricanes are leaving billions of dollars in damages in their wake, and homeowners are paying the costs in their higher insurance premiums.

Least Expensive States for Homeowners Insurance

Western states dominated the list of least expensive states for homeowners insurance, taking the top four spots, and six of the top 10. Other states in the top 10 were two Midwestern states, and two Northeastern states.

- Oregon, with an average annual cost of $706

- Utah, with an average annual cost of $730

- Idaho, with an average annual cost of $772

- Nevada, with an average annual cost of $776

- Wisconsin, with an average annual cost of $814

Western states had lower insurance premiums due to reduced exposure to hurricanes, tornadoes, and other expensive perils. Although the risk of wildfires has increased in these states recently, the majority of housing in these states is not located in wildfire zones.

Average Cost of Homeowners Insurance by City

The table below includes the average cost of homeowners insurance in 25 of the most populated cities in the United States. Among these cities, the highest homeowners insurance premiums are paid by residents of Oklahoma City, Oklahoma, with annual premiums averaging $2,795. Homeowners in Seattle, Washington paid the lowest average annual premiums, with costs averaging $555 in the city.

| City | Average Monthly Cost | Average Annual Cost |

|---|---|---|

| Austin, Texas | $78 | $934 |

| Boston, Massachusetts | $89 | $1,062 |

| Charlotte, North Carolina | $85 | $1,020 |

| Chicago, Illinois | $66 | $792 |

| Columbus, Ohio | $66 | $789 |

| Dallas, Texas | $148 | $1,780 |

| Denver, Colorado | $127 | $1,523 |

| Detroit, Michigan | $130 | $1,560 |

| El Paso, Texas | $58 | $693 |

| Fort Worth, Texas | $160 | $1,916 |

| Houston, Texas | $149 | $1,792 |

| Indianapolis, Indiana | $70 | $834 |

| Jacksonville, Florida | $72 | $864 |

| Los Angeles, California | $57 | $682 |

| Nashville, Tennessee | $91 | $1,094 |

| New York, New York | $68 | $813 |

| Oklahoma City, Oklahoma | $233 | $2,795 |

| Philadelphia, Pennsylvania | $79 | $948 |

| Phoenix, Arizona | $68 | $811 |

| San Antonio, Texas | $84 | $1,009 |

| San Diego, California | $50 | $604 |

| San Francisco, California | $51 | $608 |

| San Jose, California | $49 | $584 |

| Seattle, Washington | $46 | $555 |

| Washington, D.C. | $48 | $572 |

What’s covered by homeowners insurance, and what’s not?

Homeowners insurance provides several forms of important financial protection for homeowners. These include coverage for the building itself, a homeowner’s personal property, liability coverage for the homeowner, and other costs that a homeowner may incur in the event of a loss.

It’s important to understand that homeowners insurance generally does not cover the value of the land underneath a home. This is important for homeowners in places where land makes up a large portion of the value of a home, such as in California. Additionally, there are many exclusions from homeowners insurance policies, the most notable being earthquakes and floods.

The following are some of the key coverages included in almost all homeowners insurance policies:

- Building and fixtures. Homeowners insurance will provide financial compensation for the cost to rebuild or repair a home in the event it is damaged by a covered peril. This includes fixtures, which are items built into a home such as closet systems or cabinets. Common perils include fire, wind, rain, vandalism, theft, and many more. This is a key coverage, especially for homeowners who have a mortgage on their home, as virtually all banks will require homeowners to carry this coverage.

- Personal property coverage. Personal property is an optional coverage that is included with most homeowners insurance policies. This coverage provides financial protection for the possessions that a homeowner owns if they are damaged by a covered peril. This can include items such as furniture, appliances, and other valuables. Importantly, there may be separate, lower limits on special types of property such as jewelry, precious metals, and furs.

- Personal liability coverage. Homeowners insurance also provides personal liability coverage, which protects a homeowner in the event they are sued for causing bodily injury or property damage to another person or business. For example, if someone visits a homeowner’s property and they trip and fall and are injured, they may sue the homeowner. Homeowners insurance will pay for the cost of legal defense and any judgments or settlements against the homeowner, up to the limit of insurance.

- Loss of use coverage. If a home is damaged such that it is uninhabitable, homeowners insurance can provide loss of use coverage, which can cover the cost of rent, temporary housing, and moving costs while a home is being repaired or replaced.

What determines the cost of homeowners insurance?

A number of factors can influence the cost of homeowners insurance. It’s important for homeowners to understand what coverage they need and also to compare quotes from multiple insurance companies to get the best value for their money. Some of the most important variables that can affect premium costs paid by homeowners include:

- Location. Among the most important factors for homeowners is the location of a home. A home’s location can impact the risk of loss in several ways. The most important risk factor is weather and climate, as homes located in places where there are common weather-related or natural disaster losses generally have higher premiums. Other types of risks that can change based upon location of a home include crime levels and distance to the nearest fire hydrant and fire station, which can be an additional factor in insurance costs.

- Building construction and features. When applying for homeowners insurance, a homeowner will commonly be asked about the construction of their home, including the type of roof and foundation, the type of building material used, the number of stories in the home, and the existence of and type of basement. Additional home features can also factor into the cost, such as the presence of fire and burglar alarms, deadbolts, fire sprinklers, and more. Home construction and features that reduce the risk of damage or loss will reduce the premiums that a homeowner pays for homeowners insurance.

- Claims history and credit score. Homeowners with a history of making claims on their homeowners insurance will pay higher premiums than those with a clean claims history. Insurance companies have found that homeowners with past claims tend to be more likely to have claims in the future as well. In most states, homeowners with good credit will pay lower premiums for homeowners insurance as well, as research has shown that homeowners with good credit are less likely to have claims. In some states, the use of credit scores for insurance pricing is not allowed by state law.

- Coverage limits. Homeowners have the ability to choose coverage limits for personal property and liability coverages when purchasing homeowners insurance. The higher limits that are chosen, the more that a policyholder will pay in premiums.

- Deductibles. Policyholders have the option to choose a deductible, which is the amount the homeowner will be responsible for in the event of a loss. The deductible generally applies to the building and personal property coverages on a homeowners policy. The higher the deductible chosen, usually the lower the premium paid.

- Replacement cost or actual cash value. With regards to the personal property coverage for homeowners insurance, policyholders can choose replacement cost or actual cash value coverage. Replacement cost coverage provides funds to purchase a new version of the personal property that was damaged, while actual cash value only provides a payment for the value of the property minus any depreciation on the property. Replacement cost coverage leads to higher premiums since the potential payout is higher.

- Pets. Homeowners who have dogs may have higher premiums, because having a dog can create additional liability for homeowners. In the event that your dog causes injury or damage to another party, this can create a loss for the insurance company.

Methodology

To determine the average cost of homeowners insurance in the United States, AdvisorSmith used data published by the National Association of Insurance Commissioners (NAIC), which publishes data annually on coverages, pricing, and other trends in the insurance market. The NAIC data was taken from the 2020 NAIC Dwelling Fire, Homeowners Owner Occupied, and Homeowners Tenant and Condominium/Cooperative Unit Owner’s Insurance Report, which uses industry data from 2018.

In addition to the NAIC data, AdvisorSmith used homeowners insurance quotes from a variety of homeowners insurance companies in cities around the country. We gathered quotes for HO-3 coverage, which is the most common type of coverage for homeowners insurance in the United States. This coverage is sometimes called “all-risk” or “open-perils” coverage, as it generally covers all risks to a home that are not specifically excluded in the insurance policy.

Our average quote costs were based upon the most common type of housing in the United States, which are 3-bedroom, 2-bathroom single-family homes between 1,500 and 2,000 square feet.