Workers’ compensation insurance is an important insurance coverage that applies to many types of businesses and employers. In most states, workers’ compensation insurance is legally required for most employers, with some states offering exceptions for the smallest employers. Carrying workers’ compensation insurance protects a business financially in the event that an employee is injured while on the job.

Get a quote on Workers' Compensation

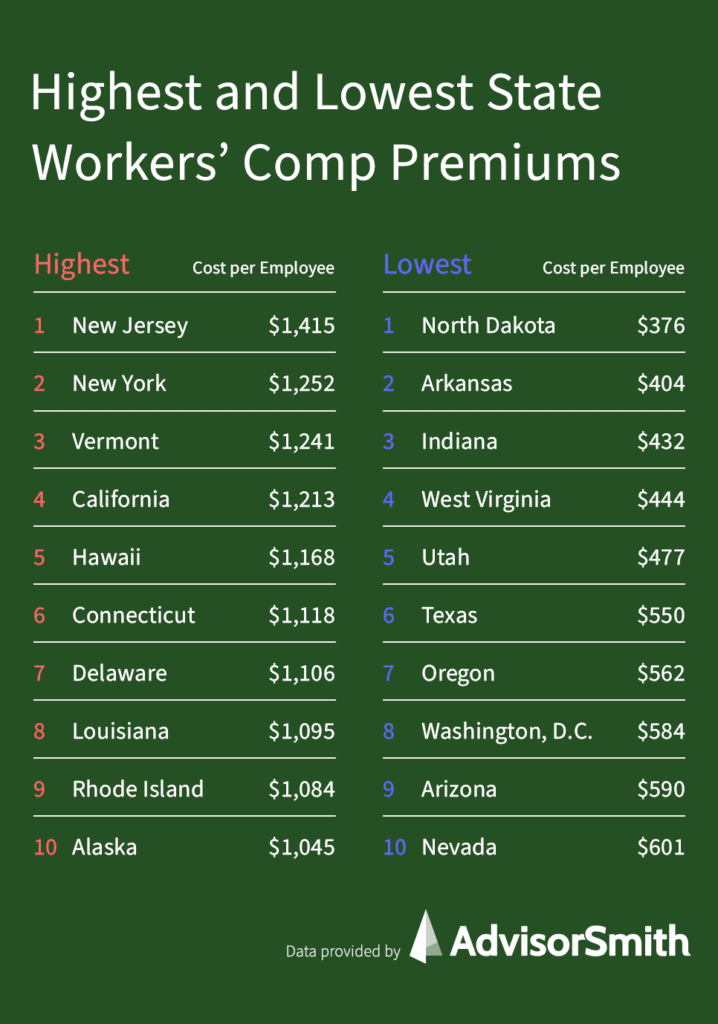

Average Cost of Workers’ Compensation Insurance

Nationwide, the average cost of workers’ compensation insurance is $936 per employee, per year, or $78 per month. The rate for workers’ compensation insurance varies considerably based upon the state, the type of business, how long the company has been in business, and the number of workers’ compensation claims a company has had. Overall, workers’ compensation premiums accounted for 1.2% of the total cost of employing the average American worker. This estimate is based on wage and premiums data from the Bureau of Labor and Statistics.

States With the Highest and Lowest Workers’ Compensation Premiums

Each state and the District of Columbia run their own workers’ compensation systems, and rules for which companies are required to have this insurance vary in each state. In many states, all companies with employees are required to carry workers’ compensation insurance, while in other states, only companies that surpass a minimum number of employees are required to have coverage. Texas is the only state in which workers’ compensation insurance is not legally required.

In most states, private insurance companies provide all or some of the workers’ compensation insurance policies available to businesses. Some states have a mixed system in which the state also runs a workers’ compensation insurance program that can be used to purchase insurance. Finally, a few states have a fully state-run system, in which workers’ compensation insurance is required to be purchased from the state.

Additionally, other factors that affect the premiums paid by businesses between states are the types of jobs and businesses within the state, the worker safety regulations required by each state, wage rates in the state, and medical costs in each state. The table below shows the states ranked highest to lowest by their average workers’ compensation costs per year and per employee, based on wage and premium data from the Bureau of Labor Statistics and the Oregon Department of Consumer and Business Services.

| Rank | State | Workers' Comp Insurance Cost per Hour | Average Annual Cost per Employee |

|---|---|---|---|

| 1 | New Jersey | $0.68 | $1,415 |

| 2 | New York | $0.60 | $1,252 |

| 3 | Vermont | $0.60 | $1,241 |

| 4 | California | $0.58 | $1,213 |

| 5 | Hawaii | $0.56 | $1,168 |

| 6 | Connecticut | $0.54 | $1,118 |

| 7 | Delaware | $0.53 | $1,106 |

| 8 | Louisiana | $0.53 | $1,095 |

| 9 | Rhode Island | $0.52 | $1,084 |

| 10 | Alaska | $0.50 | $1,045 |

| 11 | Wisconsin | $0.47 | $977 |

| 12 | Montana | $0.46 | $949 |

| 13 | Oklahoma | $0.45 | $932 |

| 14 | Missouri | $0.45 | $927 |

| 15 | Georgia | $0.44 | $921 |

| 16 | Maine | $0.44 | $910 |

| 17 | Minnesota | $0.43 | $904 |

| 18 | South Carolina | $0.42 | $876 |

| 19 | Idaho | $0.42 | $876 |

| 20 | Pennsylvania | $0.42 | $870 |

| 21 | Iowa | $0.42 | $865 |

| 22 | Washington | $0.41 | $859 |

| 23 | South Dakota | $0.40 | $831 |

| 24 | Illinois | $0.39 | $820 |

| 25 | Wyoming | $0.39 | $809 |

| 26 | Nebraska | $0.39 | $809 |

| 27 | Florida | $0.38 | $792 |

| 28 | New Hampshire | $0.37 | $769 |

| 29 | New Mexico | $0.36 | $753 |

| 30 | Alabama | $0.36 | $747 |

| 31 | North Carolina | $0.35 | $736 |

| 32 | Virginia | $0.35 | $719 |

| 33 | Colorado | $0.34 | $702 |

| 34 | Mississippi | $0.32 | $674 |

| 35 | Massachusetts | $0.32 | $657 |

| 36 | Maryland | $0.31 | $640 |

| 37 | Michigan | $0.31 | $640 |

| 38 | Kentucky | $0.31 | $635 |

| 39 | Kansas | $0.30 | $629 |

| 40 | Ohio | $0.30 | $623 |

| 41 | Tennessee | $0.29 | $612 |

| 42 | Nevada | $0.29 | $601 |

| 43 | Arizona | $0.28 | $590 |

| 44 | District of Columbia | $0.28 | $584 |

| 45 | Oregon | $0.27 | $562 |

| 46 | Texas | $0.26 | $550 |

| 47 | Utah | $0.23 | $477 |

| 48 | West Virginia | $0.21 | $444 |

| 49 | Indiana | $0.21 | $432 |

| 50 | Arkansas | $0.19 | $404 |

| 51 | North Dakota | $0.18 | $376 |

How much are workers’ compensation claims?

Workers’ compensation claims can be very costly and potentially ruinous for small businesses that don’t carry appropriate insurance. According to data from the National Safety Council and National Council on Compensation Insurance (NCCI), the average cost of a workers’ compensation claim is $41,003. Claims were generally split approximately 45% in indemnity costs and 55% in medical costs.

The most costly workers’ compensation claims were motor vehicle crashes, burns, and falls.

How are workers’ compensation premiums calculated?

The basic formula for calculating workers’ compensation insurance premiums is:

Premiums = Classification Rate x ( Payroll / $100 ) x Experience Modifier

The classification rate is a dollar amount (for example, $1.25) that is assigned to a certain type or class of workers. Most commonly, states use classifications from the NCCI to set their classification rates. Each group of workers is associated with a classification code. For example, clerical office employees are assigned classification code 8810. The classification rate reflects the average rate of employee injuries and claims for workers in that job class in a given state.

The experience modifier is a number (for example, 1.1) that is assigned to your specific company based upon the workers’ compensation claims history that your company has. Companies with safer than average working conditions for their class code will have an experience modifier less than 1, while companies with higher than average claims history will have experience modifiers greater than 1.

Unlike most types of insurance, workers’ compensation insurance rates per dollar of payroll tend to decrease over time as companies gain more experience with their work and safety improves. Companies can also improve their workers’ compensation rates by implementing training, safety procedures, utilizing personal protective equipment, and keeping their workplaces tidy and in good working order. Many insurance companies also offer free safety consulting and workplace inspections to assist in reducing companies’ risks of having a workplace injury.

Expert Commentary

Dr. Thomas Schenk is an assistant professor and director of the Environmental Health and Safety Program at Oakland University’s School of Health Sciences. Dr. Laurel Kincl is an associate professor at Oregon State University’s College of Public Health and Human Sciences. Dr. Katie Schofield is an associate professor and director of the Master of Environmental Health & Safety program at the University of Minnesota Duluth. They provided their insights on key questions regarding workers’ compensation and worker safety.

What steps can employers take to improve worker safety and health in workplaces?

Dr. Thomas Schenk: Three steps that employers can take to improve workplace safety and health are:

- Make workplace safety and health a priority in all decision-making and business processes.

- Establish health and safety committees to foster employee engagement. Listen to employee concerns and act to correct unsafe conditions or practices.

- Promote a Safety Culture where all employees take workplace safety and health seriously.

Dr. Laurel Kincl: Beyond compliance with state and federal occupational health and safety standards, employers can take additional steps to improve their workplace health and well-being. Top-down organizational strategies do not promote the necessary worker engagement needed for an effective health and safety program, but managers have a key role in supporting the systems and resources that allow health and safety managers to develop an effective program, and for demonstrating health and safety leadership.

One central step is to improve and promote effective communication. If technical skills for exposure assessment and hazard reduction exist, it is the communication piece that can truly improve the workplace. Consider that communication is related to effective training practices, reporting systems, health and safety committees, and organizational culture.

Dr. Katie Schofield: Employers should start by identifying hazards and risks that exist in their workplace and operations. How can people be injured or become ill? Activities that could cause slips, falls, strains, chemical exposures, electrocutions, being caught-in, or struck-by (including cars) would be a place to initially focus. Ideally, the hazardous conditions would then be eliminated; the goal would be to create a work environment that is 100% safe.

When this isn’t possible, work procedures and policies should be put in place to minimize workers’ exposures to hazards and protect them. Worker feedback and expertise are often the best ways to create safe, effective procedures that actually work for those using them.

Finally, establish a system or metrics to assess if safety efforts are working, and/or how they can be improved. Safety is a continuous process. Keep in mind that employers and front-line supervisors need to demonstrate support of safety efforts and practices; if they don’t, employees won’t either.

What role do individual contributors have in workplace safety and health?

Dr. Schofield: Every individual employee has a responsibility for their personal safety and ideally to look out for their co-workers. This would mean following established safety work procedures, using proper tools and equipment, reporting injuries and unsafe conditions, etc. However, if the employer does not maintain and support a safe work environment, it is unreasonable to think employees can simply “keep themselves safe.” If the worker does not have control over their work environment, or job security, or support, or protection from retaliation, then they also have little ability to individually advocate for their safety.

Dr. Kincl: While an individual contributor may not manage other people, all workers have a role in workplace safety and health. This role may be a larger role in an overall program to provide their perspective and expertise in their particular work situation and environment. The role should also include the ability to report potential hazards, near misses, and injuries, and recommend improvements without retaliation, with the ability to readily see the actions taken to address any issues.

Dr. Schenk: Individual contributors have an important role in safety and health because everyone is responsible for safety. It is up to every employee to demonstrate their commitment to workplace safety by following safe work practices and encouraging others to do the same.

Do some states or jurisdictions have more effective workplace safety regulations than others?

Dr. Kincl: State occupational safety and health regulatory programs must be at least as protective as Federal OSHA and vary in coverage of private and governmental workers. Always be aware of the state regulations and resources available. Since states have the ability to consider their typical workforces and industries, many have specific standards for specific hazardous agents or conditions.

For example, on the West Coast, both Washington and California have standards for outdoor workers and excessive heat, and Oregon is in the rulemaking process to develop such a standard. Due the risk of wildfires, California also recently passed a standard for outdoor workers and excessive smoke, and both Washington and Oregon are in the rulemaking process to develop wildfire smoke standards.

Also, some states have specific regulations that mandate effective practices such as joint labor-management health and safety committees, or additional workplace resources like consultations or trainings that promote effective practices.

Dr. Schofield: Safety regulations may be more comprehensive, or have additional requirements, in some states or jurisdictions; however, the effectiveness of any regulation is based on the ability of the individual workplace to put safety into action in real life. Safety regulations, or compliance-based safety, are often just a baseline, or bare minimum, of what must be done. For example, few regulations exist for ergonomic-related workplace risks, yet musculoskeletal injuries are a leading cause of injury. Another example is a lack of comprehensive guidance on workplace violence.

Published regulations alone won’t keep workers 100% safe, nor will they tell a workplace how to make a safety program effective. Employers that are successful with safety will use safety regulations as a guide but add additional measures based on their own workplace risks and environment. Successful employers will also have a systemic way in which they administer safety, and a method to determine if it is working, and how to keep improving.

Dr. Schenk: Compliance with safety regulations is important to maintain a safe and healthy work environment. States may promulgate safety regulations that exceed federal OSHA standards, but the effectiveness of any safety standard depends on compliance. The safety culture of the workplace determines whether safety standards are always met. Businesses with a strong safety culture may choose to adopt their own internal safety standards that exceed regulatory standards because they believe it is the right thing to do and because worker safety and health is a competitive advantage in the long run.

Methodology

To determine the average workers’ compensation insurance cost, AdvisorSmith examined workers’ compensation costs as published by the Bureau of Labor Statistics for private industry workers, which details these costs on a per-hour basis on average nationwide. We then estimated the cost for private employers if they employed a worker full-time throughout a year to find the annual and monthly costs.

AdvisorSmith also studied the workers’ compensation rates in all 50 U.S. states and the District of Columbia using data from the Oregon Department of Consumer and Business Services, which publishes an index of workers’ compensation rates by state. We applied this index to the average workers’ compensation rates to calculate an estimate of the per-worker workers’ compensation insurance premiums paid by employers in each state.

Sources

- Oregon Department of Consumer and Business Services, Information Technology and Research Section, Oregon Workers’ Compensation Premium Rate Ranking Summary

- U.S. Bureau of Labor Statistics, Occupational Employment and Wage Statistics, National Occupational Employment and Wage Estimates

- U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation

- National Safety Council, Injury Facts, Workers’ Compensation Costs